More and more property investors are seeking to improve capital values and increase rental income by renovating their properties, rather than purchasing anew.

While most investors are aware renovations can increase rental income and boost cash flow, many renovators are missing out on thousands of dollars by failing to claim depreciation deductions.

In this article we will explore:

- Are home renovations tax deductible?

- What is scrapping?

- Important legislation for property investors

- Home renovation case study

Are home renovations tax deductible?

Most residential properties have significant depreciable value, which can be claimed prior to and after home renovations are completed.

The Australian Taxation Office (ATO) allows owners of income-producing properties to claim depreciation deductions for the natural wear and tear that occurs to a building and its assets over time. Depreciation can be claimed for a building’s structure via capital works deductions and for the plant and equipment assets contained within the property.

While capital works can be claimed in both new and old residential property, plant and equipment deductions are limited to new property. This can affect what can and can’t be claimed when renovating.

Regardless of the age of the property, it’s important to speak with a specialist Quantity Surveyor before completing any work. There may be substantial depreciation deductions available for any structural elements being removed during the renovation process. This is known as scrapping.

What is scrapping?

Scrapping allows you to claim depreciation deductions for the residual value of removed assets in the year the items are removed. To take advantage of deductions for scrapped assets, a depreciation schedule must be arranged both before and after the renovation takes place. The pre-renovation depreciation schedule will detail asset values and can act as evidence in the event of an Australian Taxation Office audit.

Once the renovation has been undertaken, a Quantity Surveyor will compile an itemised schedule detailing the depreciation deductions available for the brand-new plant and equipment assets and capital improvements. The depreciation schedule will also show the undeducted value of the removed structural assets.

Important legislation for property investors

Investors who purchase second-hand residential property after 7:30pm on the 9th of May 2017 are not able to claim scrapping deductions for existing plant and equipment assets. If you exchanged contracts prior to this date, you should discuss your eligibility with a Quantity Surveyor for any residual depreciation that may apply.

If you live in your rental property while renovating, any newly installed assets will also be classed as previously used. As a result, you’ll be at risk of losing your tax benefits.

Unless there is good reason, investors who are planning on installing new plant and equipment assets should make these additions once the property has been listed for rent. This will ensure you are eligible to claim the maximum depreciation deductions available.

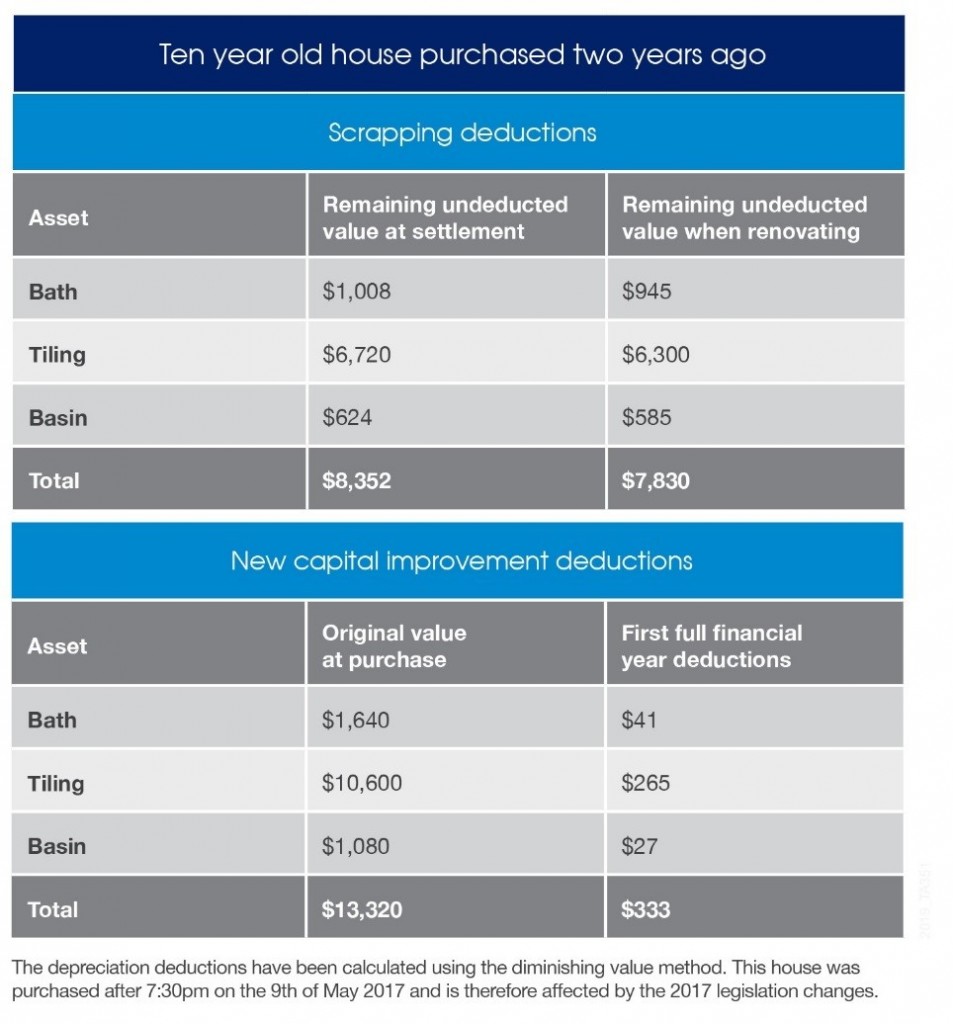

Home renovation case study

Jonathan purchased a ten year old two-bedroom house after 7:30pm on the 9th of May 2017. After renting his property out for a year, he decides to renovate the bathroom.

According to current legislation passed in November 2017, he is ineligible to claim scrapping deductions for existing plant and equipment assets. Capital works deductions for structural assets such as tiles, bathtubs, toilets, sinks and basins are unaffected by the legislation changes and can still be claimed. These deductions typically make up 85-90 per cent of a total depreciation claim.

Jonathan arranged a property depreciation schedule when he originally purchased the property. After hearing about the additional deductions available when renovating from his accountant, Jonathan contacted a Quantity Surveyor before starting work to find out more. Jonathan found he was able to use his existing depreciation schedule to work out the un-deducted value of structural assets to be removed during the renovation.

The table below outlines the deductions Jonathan could claim for the removed structural assets as well as any capital improvements made during the renovation.

After renovations, Jonathan was able to claim $7,830 in scrapping deductions and $333 in capital improvement deductions. Combined, this totals more than $8,000 in depreciation deductions in the first full financial year. He was able to maximise the depreciation deductions on his investment property both before and after the renovation.

To maximise depreciation deductions during home renovations, consult with a specialist Quantity Surveyor before getting started.