Did you know it’s possible to buy an investment property through a self-managed super fund (SMSF)? An SMSF is a private superannuation fund that can have between one and six members. All members are responsible for decisions made about the fund and compliance with the relevant legislation.

It’s common for SMSF trustees to consider purchasing investment property through their fund. However, the process is often complex, particularly when it comes to borrowing money. Before buying property through your SMSF, you must be aware of the specific rules and regulations that apply.

In this article we will look at:

Buying investment property with an SMSF

In order to buy property through an SMSF, you must abide by the following requirements.

The property must:

- Meet the ‘sole purpose test’ of solely providing retirement benefits to fund members

- Not be acquired from a related party of a fund member

- Not be lived in by a fund member or any fund members’ family

- Not be rented by a fund member or any fund members’ family.

While a property cannot be rented or lived in by a fund member or their relatives, most SMSFs are entitled to purchase their personal business’s premise, allowing the business to pay rent directly to their SMSF at the market rate. This is particularly appealing to small business owners.

Compared to other asset types, investing in property often attracts higher fees and charges which can reduce your super balance. It’s important to be aware of any fees including legal costs, stamp duty, property management expenses and bank fees before signing up.

Borrowing money when buying property with an SMSF

It’s possible to borrow money when purchasing property through an SMSF, however it must be done under strict conditions referred to as a limited recourse borrowing arrangement (LRBA).

An LRBA involves an SMSF member taking out a loan to purchase a single asset, in this case a property, which is held in a separate trust. Any investment returns earned from the property go to the fund. If the SMSF defaults on the loan, no other assets within the SMSF are affected. A personal guarantee can be required so the individual’s assets could be affected.

The SMSF generally needs to have a minimum balance of $180,000 to be able to purchase a property and an annual contribution of at least $15,000. In addition, most lenders require an SMSF to have at least 30 per cent of the value of the property as a deposit and often charge a higher rate of interest.

As borrowing to invest can sometimes be considered high risk, it’s best to discuss your borrowing options and LRBA with a trusted financial adviser.

Recent laws affecting SMSFs

Concessional contributions are the funds that go into your super account from your before-tax income. The concessional contribution limit is now set at $27,500 , while the after-tax or non-concessional limit is $110,000 . Individuals can make extra concessional contributions above the $27,500 limit if they have haven’t used the entire concessional cap amounts from previous years. To use an unused cap, the individual’s total super balance must be less than $500,000 at the end of 30 June the previous financial year and have made concessional contributions in the financial year that exceeded the individual’s general concessional contributions cap.

Individuals can re-contribute amounts they withdrew between 1 July 2021 and 30 June 2020 under the COVID-19 early release of super program without them counting towards their non-concessional contributions cap.

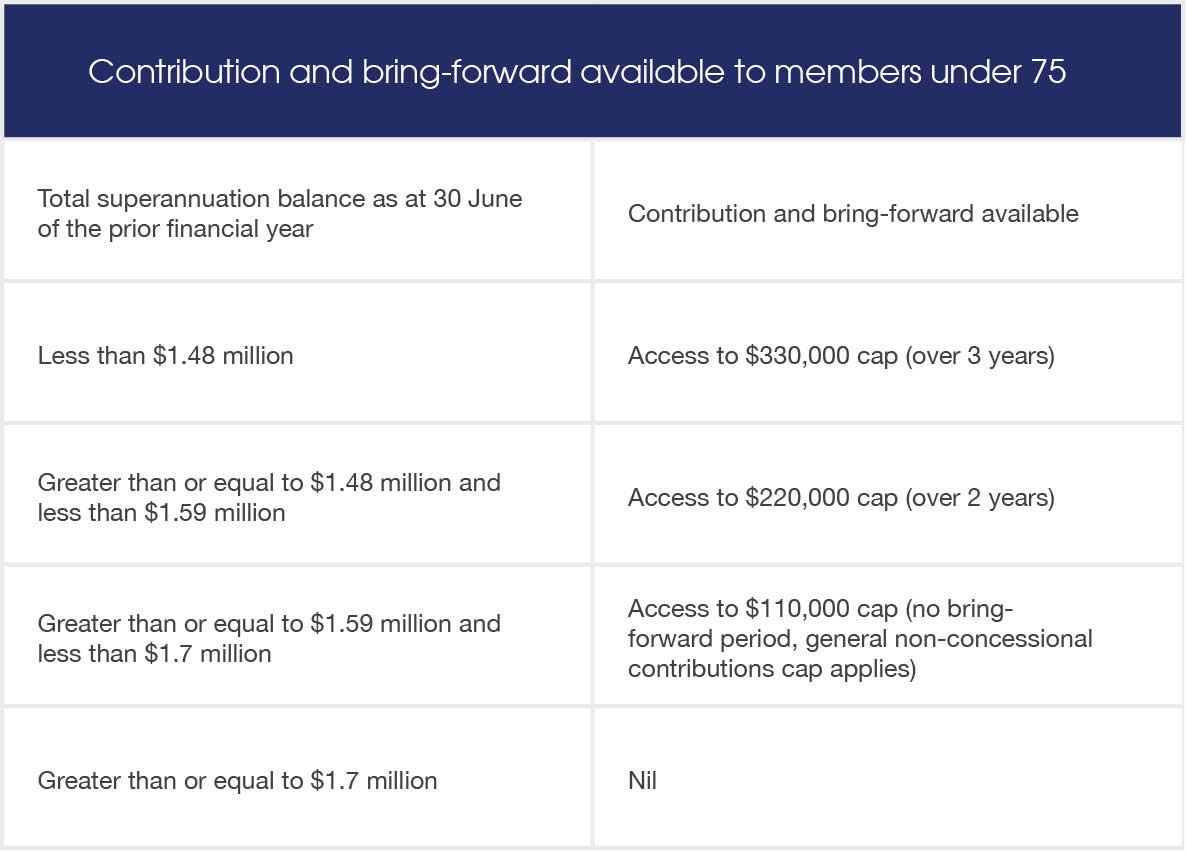

The ‘bring-forward rule’ allows a trustee to contribute up to three years’ worth of non-concessional contributions in one year.

From the 2022–23 financial year members who are under 75 may be able to access a bring-forward arrangement as outlined in the table below.

The way the ATO calculates a trustee’s total super balance (TSB) has also changed. In certain circumstances, an individual’s LBRA amount will be factored into their TSB if the loan contract was entered into on or after 1 July 2018. This will apply if:

- The LBRA is with an associate (relative, other member of SMSF, partner or company) of the fund. All members of the fund whose interest is supported by the asset purchased using the loan must include the LBRA in their TSB calculations.

- A member of the fund met a condition of release with a nil cashing restriction.

If your TSB is greater than $1.7 million from 2021-22, you can no longer make non-concessional contributions.

The ATO also made changes to the way an SMSF can buy assets such as property. A property purchased through an SMSF must be done on an ‘arm’s-length basis’, meaning that a transaction made by the fund must reflect the true market of the asset.

Any income made from that asset must also reflect the true market rate of return. For example, an SMSF trustee cannot purchase a house to be rented by their son at a lower rental rate. If there is not adequate documentation to prove the money provided by a related party was actually borrowed, the amount provided by the related party might be considered to be a contribution received by the fund. This could lead to significant tax consequences if it results in a contributions cap being exceeded.

Can you claim depreciation for an SMSF investment property?

There are tax implications when the trustees of an SMSF choose to invest in real estate. As with any other property investment, SMSF trustees who invest in real estate are entitled to claim capital works deductions for the wear and tear of a building’s structure as well as depreciation for any eligible plant and equipment items.

It’s important that SMSF trustees take advantage of the additional funds available via a depreciation claim. BMT Tax Depreciation can prepare depreciation schedules for trustees with an investment property to help maximise their claims.

You might also enjoy reading:

Can rooming houses be purchased under SMSF.

All required points covered, when buying a property with an SMSF, beautifully explained!

Very good read. Thanks for sharing.

Hi,

It says you can have 4 or less members, can me and my husband be in one SMSF?

Hi BMT team,

If SMSF borrowers to purchase investment property does this borrower impact personal lending capacity of the borrower?

Hi Fouad,

Thanks for your comment.

You are best to seek advice from your lender or mortgage broker as it may depend on the type of SMSF loan that was established and whether any personal guarantees were provided for this loan.

This may impact your borrowing capacity if so, however, because we’re only specialised in tax depreciation, we can’t provide advice.

Thanks,

The BMT Team.

Is it possible for a SMSF to purchase a trustee’s property but the trustee not live at the property after the sale?

Hi Liz,

Thanks for your comment.

A SMSF can’t purchase a residential property from a trustee in any circumstances.

A property purchased by a SMSF also cannot be lived in by any trustee or anyone related to the trustees.

Thanks,

The BMT Team.

Hi, is it possible to buy a SMSF investment property with siblings?

Hi Vanessa,

No, the relevant legislation prohibits SMSFs to purchase an investment property with a related party.

For more information, we recommend consulting your accountant or financial adviser.

Thanks,

The BMT Team.

Hi BMT,

Has the ability for a SMSF to claim depreciation for an investment property that is not brand new build changed since this article?

With thanks,

Brigid.

Hi Diana,

Thanks for the comment.

Capital gains tax is calculated by deducting the proceeds from the cost base at the time of selling and apportioned over the time it was used to produce an income. There is a fifty per cent CGT discount for properties owned longer than twelve months.

You may find this article on capital gains tax helpful: https://www.bmtqs.com.au/maverick/mav-52-depreciation-and-cgt

Because we’re only specialised in capital gains tax as directly related to tax depreciation, we recommend consulting an accountant or financial advisor.

Thanks,

The BMT Team.

Hi Brigid,

Thanks for your comment.

Depreciation eligibility within SMSF properties hasn’t changed.

This article has recently been updated including any changes to SMSF laws and regulations mentioned throughout.

Thanks,

The BMT Team.