The Australian Government introduced temporary full expensing in 2020 to stimulate business investment and drive economic growth during the pandemic. The incentive was put in place until 30 June 2023, to support the country’s economic recovery from the impacts of COVID-19.

Given that temporary full expensing will not be extended past this date, businesses wanting to take advantage of the incentive have until the end of financial year 2022-23 to purchase and install qualifying assets and claim the costs in the same financial year.

What is temporary full expensing?

Temporary full expensing was developed to encourage businesses to invest in new assets such as new equipment, machinery, and technology. Under the scheme, eligible businesses can claim an immediate deduction for the full cost of qualifying depreciable assets, rather than claiming deductions over several years.

Temporary full expensing is essentially a supercharged version of the instant asset write off, originally introduced in 2015, and applies to more businesses and to a broader range of assets. It allows eligible businesses to immediately deduct the full cost of qualifying assets of any value in the year they are first held, and first used or installed ready for use for a taxable purpose.

Overview of eligibility

Businesses may be eligible for temporary full expensing if they have an aggregated turnover of less than $5 billion or are a tax entity that meets the alternative income test.

For the 2020-21, 2021-22 and 2022-23 income years, an eligible entity can claim in its tax return a deduction for the business portion of the cost of:

- eligible new assets first held, first used or installed ready for use for a taxable purpose between 7.30 pm AEDT on 6 October 2020 and 7:30 pm AEDT on 30 June 2023

- eligible second-hand assets where both:

– the asset was first held, first used or installed ready for use for a taxable purpose between 7.30 pm AEDT on 6 October 2020 and 30 June 2023

– the eligible entity’s aggregated turnover is less than $50 million

- improvements incurred between 7.30 pm AEDT on 6 October 2020 and 30 June 2023 to

– eligible assets

– existing assets that would be eligible assets except that they are held before 7.30pm AEDT on 6 October 2020

- eligible assets of small business entities using the simplified depreciation rules and the balance of their small business pool.

Capital works (Division 43) deductions are not eligible to be claimed under this incentive.

Changes to small business support

While temporary full expensing hasn’t been extended, the instant asset write-off will continue to support small businesses.

The instant asset write-off threshold has been temporarily extended to $20,000 from 1 July 2023 until 30 June 2024. Small businesses with an aggregated turnover of less than $10 million, will be able to immediately deduct the full cost of qualifying assets costing less than $20,000 that are first used or installed ready for use between 1 July 2023 and 30 June 2024.

The threshold will be applied on a per-asset basis, which means small businesses can instantly write off multiple assets. Assets valued at $20,000 or more (which cannot be immediately deducted) can continue to be placed into the small business simplified pool and depreciated accordingly. The provisions that prevent small businesses from re-entering the simplified depreciation regime for five years if they opt out will continue to be suspended until 30 June 2024.

Small businesses with an aggregated turnover of less than $50 million will also have access to a bonus twenty per cent tax deduction up to a maximum of $20,000 ie up to $100,000 of total expenditure for eligible assets supporting electrification and more efficient use of energy, from 1 July 2023 until 30 June 2024 under the newly introduced Small Business Energy Incentive. Further detail on the application of this incentive and the eligible assets will be forthcoming.

How businesses can benefit from temporary full expensing until 30 June 2023

Temporary full expensing is seen as a powerful tool to encourage businesses to invest in new equipment, machinery, and technology, as it lowers the cost of investment and provides an immediate tax benefit.

Although the incentive is a short-term measure, it has the potential to create long-term economic benefits by increasing productivity and boosting employment.

For businesses, upgrading equipment or machinery can increase efficiency and output, which could lead to increased revenue and profitability in the long run.

It’s important businesses act fast if they’d like to ensure deductions are immediate as assets must be purchased and installed ready for use by June 30.

We take a look at how a business’s cash flow can be affected by applying temporary full expensing and in a second scenario the outcome of a business opting out .

Case studies

The business used in these scenarios is a medium-sized business entity and completed renovations and upgrades towards the end of 2022.

Scenario one: Business applies temporary full expensing

A business upgraded various equipment and machinery throughout their office including computer equipment and systems, desk fit-outs, kitchen appliances, photocopiers and printers, telephone systems and office waste and recycling tools.

The business was due for upgrades and saw temporary full expensing as the perfect opportunity to do so.

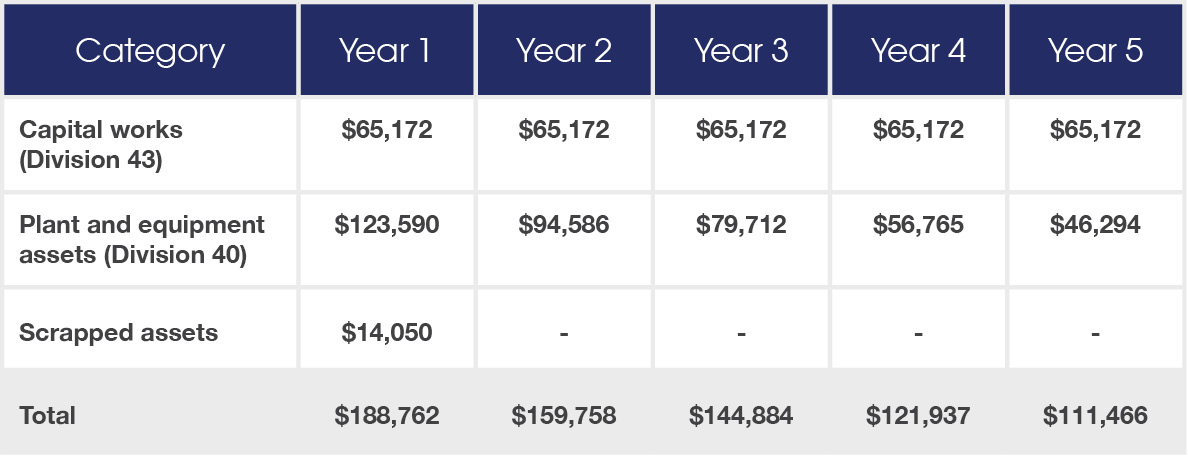

The following table demonstrates the five years’ cumulative depreciation deductions following the upgrades. The table also displays the deductions for the scrapped assets in year one.

Capital works aren’t affected by the incentive but are included to display accurate total deductions within this scenario.

The deductions for plant and equipment assets occurring from years two to five are existing assets still generating deductions which the business retained.

The immediate deduction for qualifying assets in year one not only boosted cash flow for the business but also offset a large tax liability. The upgrades allowed the business to also increase productivity and improve its energy rating due to the more energy-efficient equipment.

Scenario two: Business opts out of temporary full expensing

The business upgraded various equipment and machinery throughout their office including computer equipment and systems, desk fit-outs, kitchen appliances, photocopiers and printers, telephone systems and office waste and recycling tools.

The business chose to opt out of temporary full expensing and claimed deductions normally using the diminishing value method of depreciation.

Because the business opted out of the scheme, their deductions were more consistent over the five years.

As we can see in this scenario the business claimed deductions consistently over multiple years rather than immediately, still improving cash flow and lowering its tax liabilities every year.

The same total deductions will be claimed in both scenarios, however, provide different short- and long-term cash flow outcomes.

Applying this incentive won’t be a suitable approach for all commercial business operators, so, it’s important to discuss the potential gains and losses with an accountant or financial advisor before deciding.

Business owners who are anticipating a large tax liability, due for upgrades, and want to improve cash flow and increase productivity have until 30 June to take advantage of temporary full expensing.

Australian businesses can best take advantage of temporary full expensing with a BMT Tax Depreciation Schedule, which identifies all assets and maximises deductions. BMT take all business incentives into account and apply them to qualifying assets when applicable.

To learn more about how temporary full expensing can improve cash flow, call the experts on 1300 728 726 or Request a Quote.