The new financial year welcomed Tax Ruling (TR) 2021/3 to the Australian taxation framework. This new public TR has been in place from 1 July 2021 and relates to the effective life of depreciating assets. Here is what you need to know.

What is a public tax ruling and why are they important?

Australia’s public tax ruling system allows the Tax Commissioner (the Australian Taxation Office) to introduce binding rules and advice for all Australian taxpayers to follow.

Tax rulings are an essential part of the nation’s taxation system and fill the gaps that are left by tax laws in place.

Tax rulings can be public or private and TR 2021/3 is an example of a public ruling. This ruling is critical to the depreciation landscape as it is focussed on the effective life of depreciating assets.

What does tax ruling 2021/3 relate to?

In short, TR 2021/3 addresses the effective life of plant and equipment assets. This particular ruling also introduces rates for assets in the salt harvesting and horse training (racing) industries, which weren’t previously specified.

Plant and equipment assets are those that are easily removable or mechanical in nature like furniture, motors and tools. Each plant and equipment asset has a designated effective life set out by this ruling which determines its depreciable rate.

New industry in TR 2021/3: Salt harvesting

On average, the Australian salt harvesting industry produces approximately 12.2 million tonnes of salt annually, with most of this coming from Western Australia. Previously, there was no allowance for salt harvesting assets in tax rulings, making TR 2021/3 important to the industry.

Just some of the assets that have been added in the ‘salt harvesting’ industry class include culverts for conveying seawater/brine/bitterness, tugboats, trucks, port assets and pumps. Assets such as these each have an effective life that’s set to be suitable for the new industry class in TR 2021/3.

New industry in TR2021/3: Horse training (racing)

The second industry that was introduced in TR 2021/3 was horse training (racing). Many of these assets fell under other categories previously, but some have also been added to appropriately reflect assets and their uses in this industry.

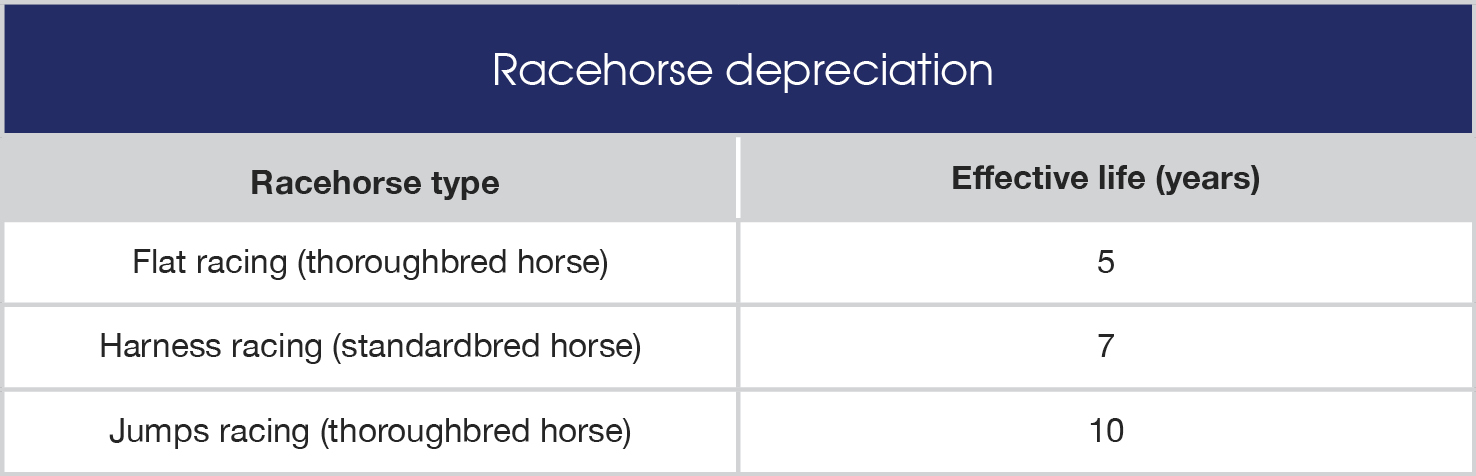

For example, a ‘racehorse’ was previously depreciated under sport and recreation services with an effective life of ten years. But with this new industry included, ‘racehorse’ has been split into the different type of trained horses as demonstrated in the table below.

Other assets that fall under this category include support assets like horse floats and rugs, portable assets, horse training pools, lead companion ponies and tack room furniture.

What does BMT do when a new tax ruling is introduced?

BMT have multiple processes in place to guarantee that every BMT Tax Depreciation Schedule is 100 per cent compliant.

All changes that are made in a public tax ruling is applied and adopted when preparing a schedule, ensuring that every deduction is captured.

To learn more about depreciation and how BMT helps investors claim maximum depreciation deductions while maintaining full compliance, contact the team on 1300 728 726.