Given that median house and unit prices have continued to rise in some areas of the property market during 2016 and in Sydney and Melbourne in particular, it’s no surprise to learn that more investors are choosing to take advantage of co-ownership.

Recent figures from Mortgage Choice show an increase in first home owners

co-buying with friends and family, up from 7.9 per cent to 9.2 per cent.

Investors too are also taking advantage of the benefits which co-ownership can provide them, such as increasing their buying power by combining their income and savings, improving borrowing capacity and reducing the burden of the corresponding expenses involved in holding the property.

Given it is the season for sharing, we thought we would provide details about how co-ownership will not only make it easier to invest in property, but also explain how this can affect the depreciation deductions investors can claim.

To ensure that depreciation claims are correct and maximised, investment property owners are encouraged to speak with a specialist Quantity Surveyor to request a tax depreciation schedule for their property. If a property has more than one owner, it is recommended to select a depreciation schedule provider, such as BMT Tax Depreciation, who outline deductions based on each owner’s percentage of ownership in each individual asset.

By splitting an assets value by ownership percentage first, each investor potentially will qualify for higher depreciation deductions.

Split schedules enable co-owners to increase deductions for plant and equipment items earlier in their effective lives using depreciation methods such a low-value pooling and immediate write-off.

Let’s take a look at each of these methods and explain how these should be calculated for assets which are found within a property with a 50:50 ownership split.

Low-value pooling

Low-value pooling is a method of depreciation which allows an investor with an ownership interest in an asset of less than $1,000 in value to claim deductions at an accelerated rate of 18.75 per cent in the year of purchase and 37.5 per cent each year afterwards. As each investor’s ownership interest may qualify for the low-value pool, co-ownership expands the number of items that can be claimed at this higher rate of depreciation. For example, in a 50:50 ownership situation, items valued less than $2,000 can be written off immediately.

Immediate write-off

Legislation allows property investor’s to claim an immediate write-off for assets with an opening value of $300 or less. In a situation where ownership is split between one or more parties, the rule allows investors to claim an immediate write-off to items where an owner’s interest in the asset is less than $300. For example, in a 50:50 split scenario, items valued less than $600 can be written off immediately.

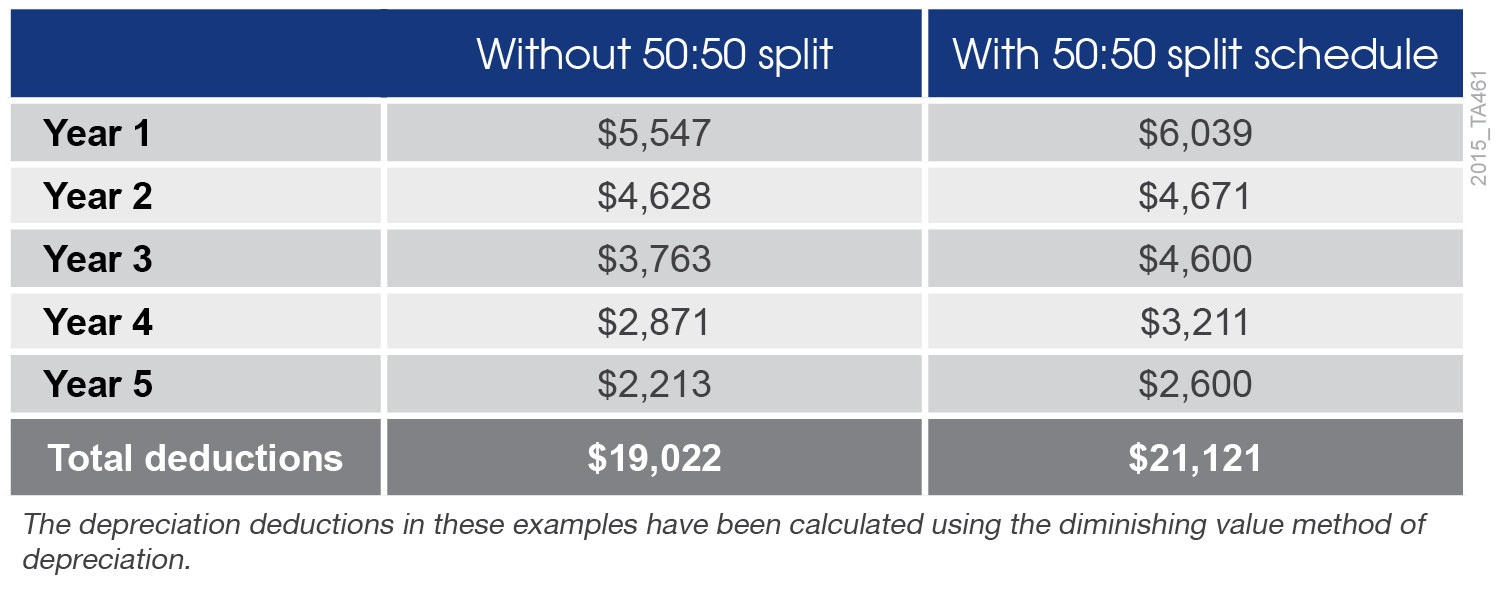

Example scenario

Below is an example of the difference obtaining a split depreciation schedule will make for two investors who co-buy an investment property with a 50:50 split.

As you can see, in the first financial year alone the owners can claim an additional $492 by requesting a depreciation schedule with a 50:50 split. Over five years of cumulative claims, the total difference for the owners in their deductions using the split schedule is $2,099.

The increase in depreciation deductions helps owners to greater improve their tax returns and therefore their cash flow.

Whether you’re an investor with just one property, an investor who purchases an investment property with your partner in a 50:50 split, or even if it is for four owners who choose to split deductions at 70:15:10:5, a comprehensive depreciation schedule which is tailored for the investors needs and considers the property owners circumstances will provide additional cash flow.

This extra money really can come in handy to help with holding costs throughout the year, or even be beneficial for the owner at Christmas time, when any savings may just help you and your family to share some of the festivity around your Christmas tree.