When you use a property for investment purposes, you want it to increase in value, or appreciate, over time. So why consider depreciation?

While the value of the property hopefully rises during ownership, the building structure and assets within it will experience natural wear and tear. The Australian Taxation Office (ATO) allows owners of income-producing properties to claim depreciation deductions for this natural wear and tear.

These deductions can be claimed under two categories – capital works deductions and plant and equipment depreciation.

Capital works deductions refer to the building’s structure and items considered to be permanently fixed to the property such as kitchen cupboards, doors and sinks. Residential homes in which construction commenced after 15 September 1987 are eligible to claim capital works deductions at a rate of 2.5 per cent over forty years.

Plant and equipment assets are items which are easily removable from the property such as carpet, hot water systems and blinds. These assets have a limited effective life as set out by the ATO and can generally be depreciated over time.

While almost all property investors will be able to claim depreciation, those who build a new property will usually claim higher deductions.

Benefits of building a new investment property

There are two main tax benefits to building a new investment property:

- Unlike an owner of second-hand real estate, an investor who builds a new property is not affected by legislation changes passed in November 2017. These changes eliminated the ability to claim a deduction for previously used plant and equipment assets found in second hand or previously owner-occupied residential investment properties. Owners of new property are still entitled to claim depreciation deductions for all eligible plant and equipment assets found within their property.

- The owner of a new property is eligible to claim a deduction for the entire cost of the building structure over forty years. Owners of existing property can only claim the remaining years available.

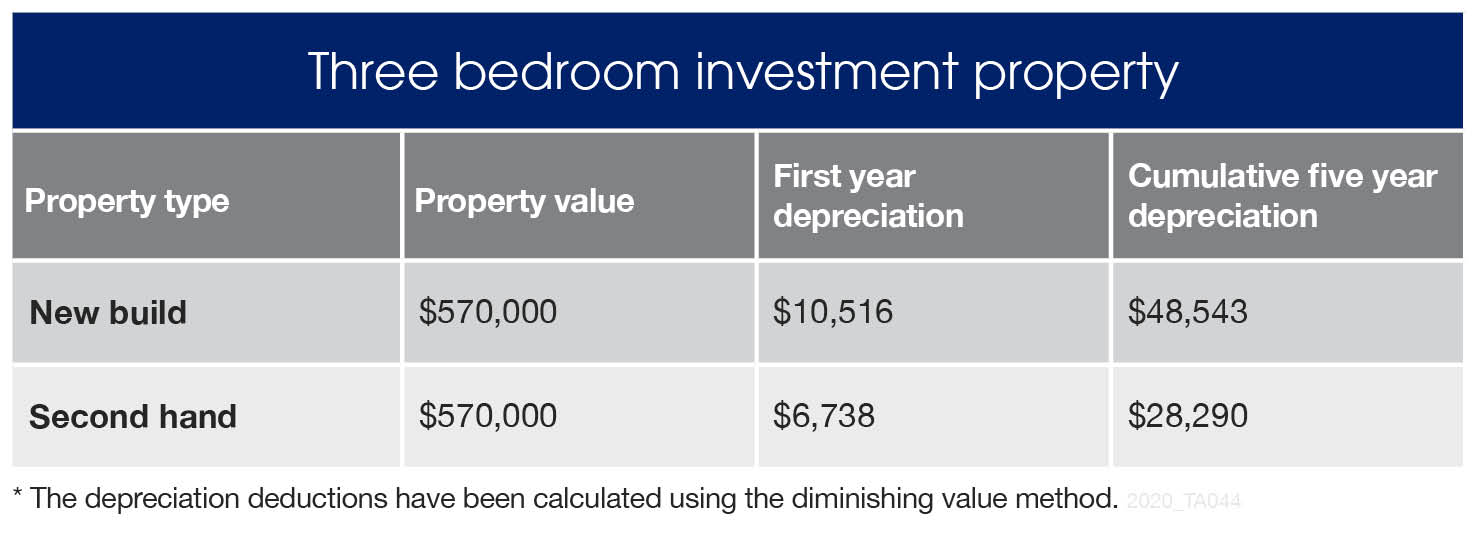

The table below shows the first full financial year depreciation deductions and the five-year cumulative depreciation deductions for a new build and a second-hand property, both valued at $570,000.

The newly built property is entitled to a first-year deduction of $10,516, while the second-hand property offers $6,738. Over the five years, the new property will allow the owner to claim $48,543 and the second hand will provide more than $28,000. While the second-hand property still offers lucrative deductions for the owner, there are clear benefits to owning a new investment property.

Along with depreciation, there are several other benefits of a newly built investment property. A new home will attract an abundance of tenants seeking low maintenance, neat and tidy properties with urban convenience. As a result, the property is likely to provide consistent weekly rental returns and a low vacancy rate depending on the location and current market.

When you are building an investment property from scratch, you’re also able to cater to the current market. Research what rental properties are performing well, considering the floor plan and key features that tenants are willing to pay a premium for. This could help you earn higher rental income and increase the value of the property over time.

Depreciation case study: building an investment property

Let’s analyse another example to highlight the importance of claiming depreciation as an investor. John builds a three-bedroom investment property for $600,000. From the property, he earns a rental income of $545 per week or a total income of $28,340 per annum. Expenses for the property such as interest, rates and management fees total $39,067.

The following scenario shows John’s cash flow with and without depreciation.

BMT Tax Depreciation found John $11,200 in the first financial year alone. Without depreciation he was paying an annual outlay of $6,758 per annum or $130 per week. By claiming depreciation, John reduced his outlay to $2,614 per annum or $50 per week. That’s a difference of $80 per week, or $4,160 for the first full financial year.

To find out how much you could be claiming each year, Request a Quote or contact BMT on 1300 728 726 today.

Hi

I purchased an investment property on May 2021 brand new home, I am still awaiting depreciation schedule, What are my options in terms of tax. Due to lockdown and restriction . the depreciation report may take much more longer to complete but I need to do tax soon. Can I claim depreciation next year or I have to claim this year

One more question, is stamp duty on investment claimable in tax?

Thank you

Tej

Hi Tej,

Thanks for your comment.

We are experiencing some delays due to lockdown restrictions, but please rest assured as soon as restrictions are lifted and its safe to do so we will be prioritising delayed jobs.

In terms of tax, a BMT Tax Depreciation Schedule allows you to amend previous tax returns. This means even if you don’t get your schedule in time for this year’s tax return, you will still be able to claim depreciation for the 2020/21 financial year by lodging an amendment.

However, stamp duty isn’t tax deductible as it forms part of the property’s cost base.

Thanks,

The BMT Team

Hi BMT,

I built a new property and put it on the market for rent. However, after a month I decided to move in instead.

Am I able to claim any depreciation deduction for the property during the time it was on the rental market?

Thanks

Hi Natalie,

Thanks for your comment.

We will need to look at several factors to determine whether you can claim depreciation for the month the property was on the rental market.

For example, if the property was classed as genuinely available for rent as per the ATO’s standards then depreciation may be available. However, not actually receiving income from the property may also impact this. You can find more information on the ATO’s standards here https://www.ato.gov.au/Individuals/Investments-and-assets/Residential-rental-properties/Rental-property-genuinely-available-for-rent/

You also need to consider the impact the small amount of deductions could have on your future CGT implications. We recommend to seek further advice from an accountant.

Thanks,

The BMT Team